Endowments and foundations with similar portfolio structures are increasingly producing very different returns. This divergence is not driven by a fundamental shift in allocation. Alternatives have long been a core driver of institutional portfolio returns.

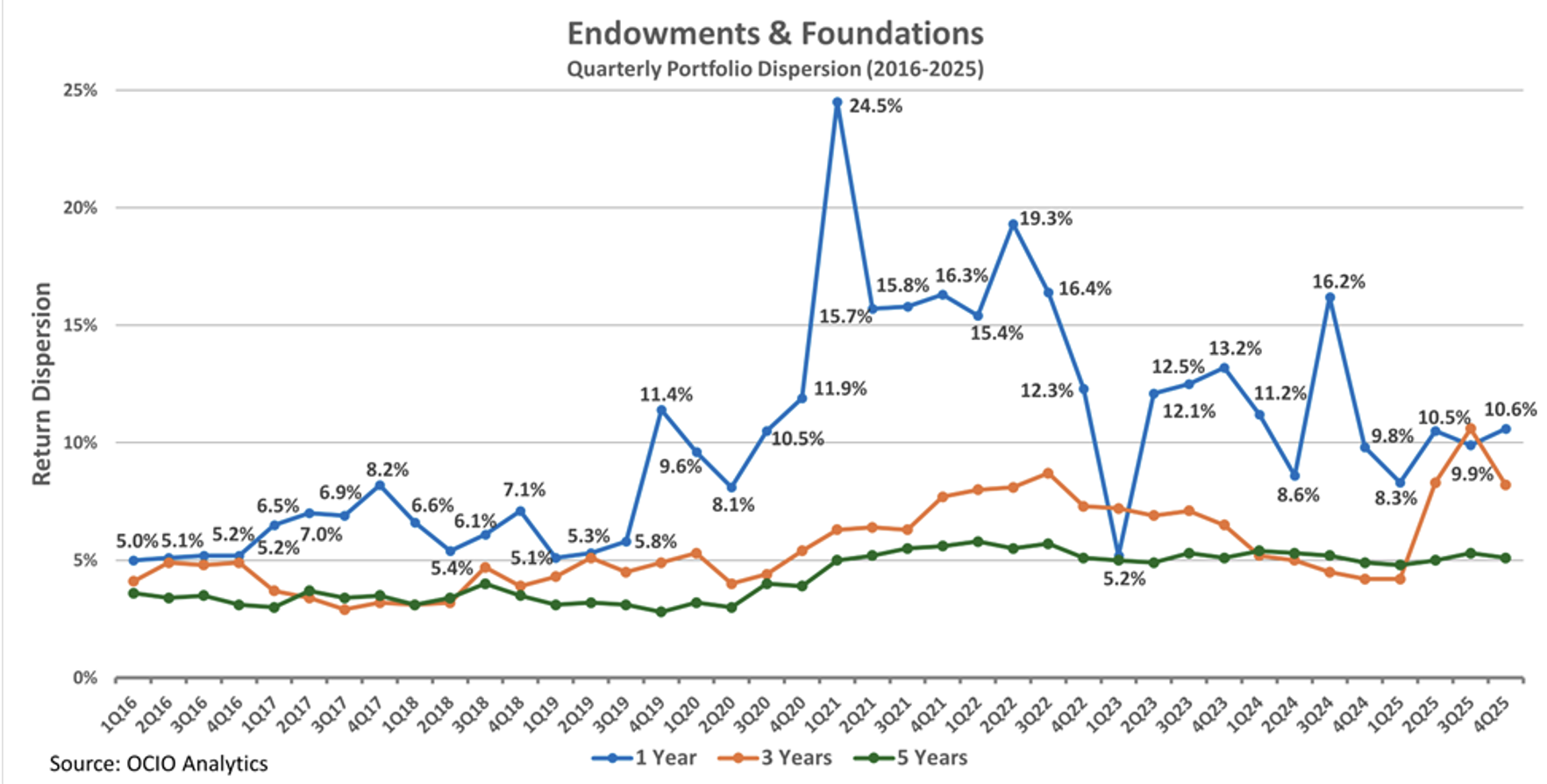

The data bears this out. Across portfolios tracked by OCIO Analytics, return dispersion—defined as the spread between the 5th (top-performing) and 95th (lowest-performing) percentiles of returns across institutions—has been structurally elevated since 2020, peaking at 24.5% in 1Q21 and remaining above pre-2020 levels through 4Q25. Even on a smoothed 5-year basis, it has held above 5% throughout the period. This is not cyclical variation; it reflects a structural shift in the implementation environment.

The answer lies not in the presence of alternatives, but in how they are selected, constructed, and implemented. In this environment, measuring implementation is no longer optional—it is essential.

Why Allocation Alone Does Not Explain Higher Dispersion

A common narrative is that dispersion has increased because institutions have allocated more to private markets and other alternatives. That explanation is incomplete. Endowments and foundations have relied on alternatives for decades to enhance returns and diversification.

If allocation alone were the driver, dispersion would have been elevated historically. It was not. The structure has remained broadly consistent. What has changed is the range of returns within that structure.

Alternatives Are High-Dispersion Asset Classes

Most investment committees understand that alternatives behave differently than public equities and bonds. What is less well understood is the sheer magnitude of manager dispersion within alternatives, and therefore how much of a portfolio’s returns hinge on implementation rather than allocation decisions.

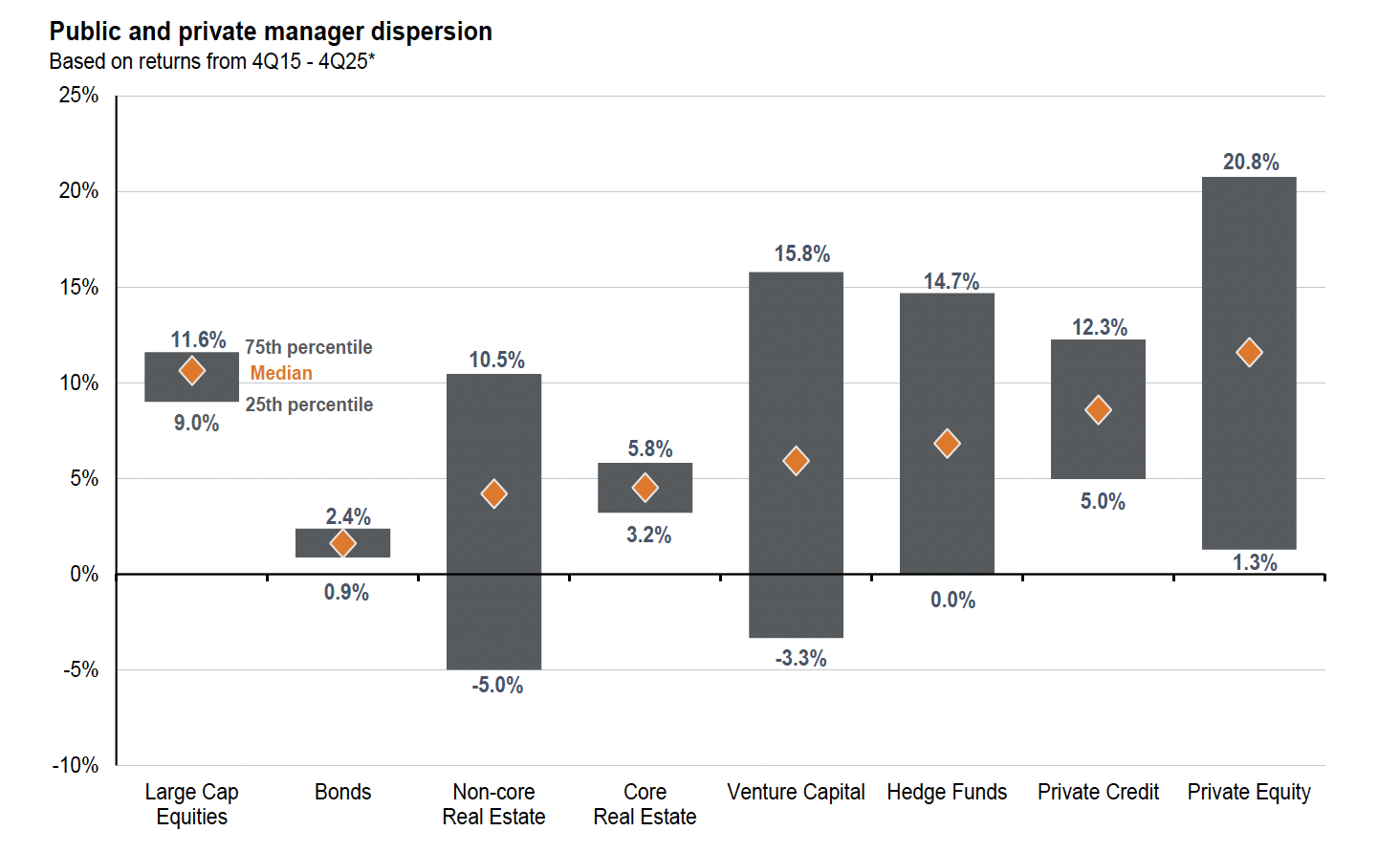

The data is striking. Across asset classes over the 10-year period ending 4Q25, the spread between 25th and 75th percentile managers tells a very different story:

Source: JP Morgan Asset Management

Source: JP Morgan Asset Management

The contrast is stark. Large-cap equities produce a 25th-to-75th percentile spread of just 2.6 percentage points. Bonds are similarly tight at 1.5 points. But move into alternatives and the picture changes dramatically: private equity spans 19.5 percentage points, venture capital 19.1 points, and hedge funds 14.7 points.

For an endowment or foundation allocating 30–40% of its portfolio to alternatives, this is not a marginal consideration. It is the dominant driver of returns. Two portfolios with identical allocations can experience returns that differ by double digits—not because of what they own, but because of how well it was implemented.

The asset class is not the risk. The manager is.

Conclusion

Alternatives have been, and remain, the primary driver of top-quartile performance for endowments and foundations. What has changed is not the relevance of alternatives, but the environment in which they are implemented. The opportunity set is broader, manager dispersion is wider, strategy complexity is greater, and capital flows into private markets have expanded significantly.

As a result, similar portfolios no longer produce similar returns. Allocation still matters, but it no longer fully explains differences in returns among institutions with comparable portfolio structures. Implementation does.

Follow Us

Follow Us