Summary

- Institutional portfolios pursuing similar strategies can diverge by hundreds of millions of dollars over a decade, driven less by strategy than by when underperformance occurs.

- Return dispersion across endowment and foundation portfolios frequently reaches double-digit spreads in a single year, turning small annual performance differences into permanent wealth gaps through compounding.

- The Dispersion Trap is structural: losses during high-dispersion periods are hard to recover once dispersion compresses.

Introduction

Many endowments and foundations pursue broadly similar investment strategies. They allocate across public equity, private markets, real assets, diversifying strategies, and fixed income, often with comparable long-term targets. Yet over time, their outcomes are anything but similar. This divergence is often attributed to strategic asset allocation. In reality, a significant portion of outcome differences emerges from dispersion—the widening and narrowing of returns across otherwise similar portfolios.

When dispersion is elevated, relatively small differences in performance compound into permanent gaps in institutional wealth. When dispersion compresses, those gaps become difficult, if not impossible, to close. This dynamic creates what we call the “Dispersion Trap”.

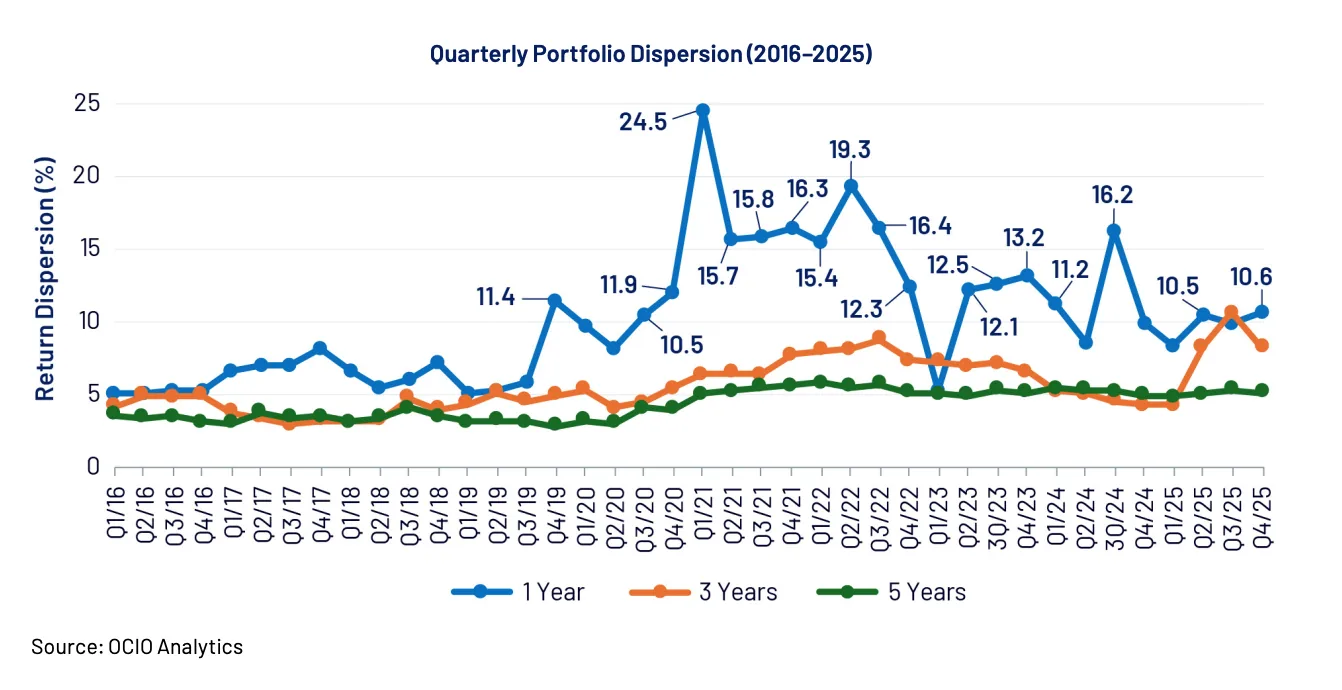

Dispersion in this paper is defined as the spread between the highest- and lowest-performing portfolios, measured using the 5th (top-performing) and 95th (lowest-performing) percentiles of returns across institutions in the OCIO Analytics dataset.

Even among portfolios implementing similar “endowment-style” frameworks, realized results can differ significantly. Few institutional studies explicitly analyze dispersion across endowment-style portfolios, yet dispersion is one of the most powerful drivers of long-term outcome differences.

Economic Impact of Dispersion

Small differences in annual returns can compound significantly over time. For long-horizon investors such as endowments and foundations, even modest return differences can translate into large gaps in institutional wealth.

The economic implications of dispersion become particularly clear when examining the long-term compounding effects of relatively small return differences. The impact of dispersion is easiest to see in dollar terms.

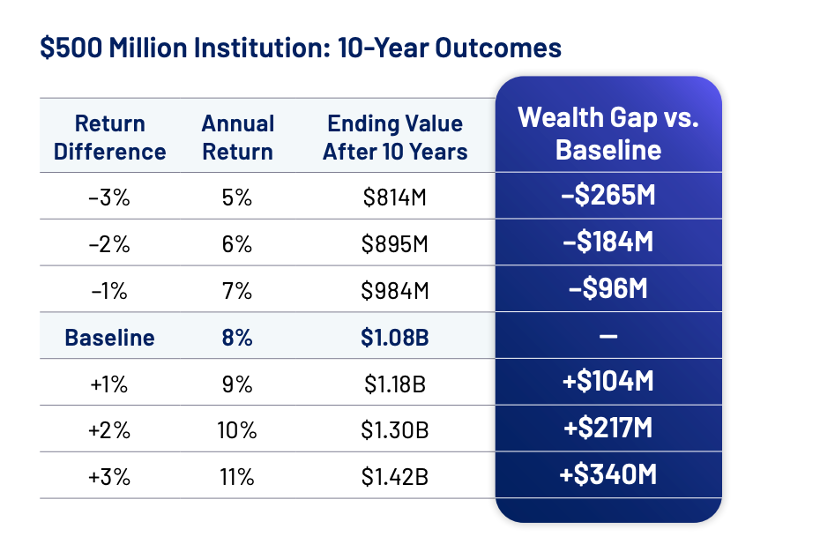

A $500 million portfolio earning just 1% less per year than peers finishes the decade with $96 million less wealth, while a portfolio earning 1% more annually generates more than $104 million of additional capital.

Dispersion Across Institutional Portfolios

Data from the OCIO Analytics dataset shows that dispersion frequently reaches double-digit levels over one-year periods and remains meaningful even across longer horizons. While dispersion narrows over time, it does not disappear—leaving a lasting impact on outcomes.

When Dispersion Widens

Dispersion often increases during periods of market stress, asset-class divergence, or major shifts in economic conditions. During these environments, implementation decisions—such as manager selection, private-market exposure, or liquidity positioning—can amplify performance differences across portfolios. These environments often create the largest opportunity for institutional portfolios to diverge in long-term outcomes.

The Dispersion Trap

The interaction between dispersion and compounding creates the Dispersion Trap:

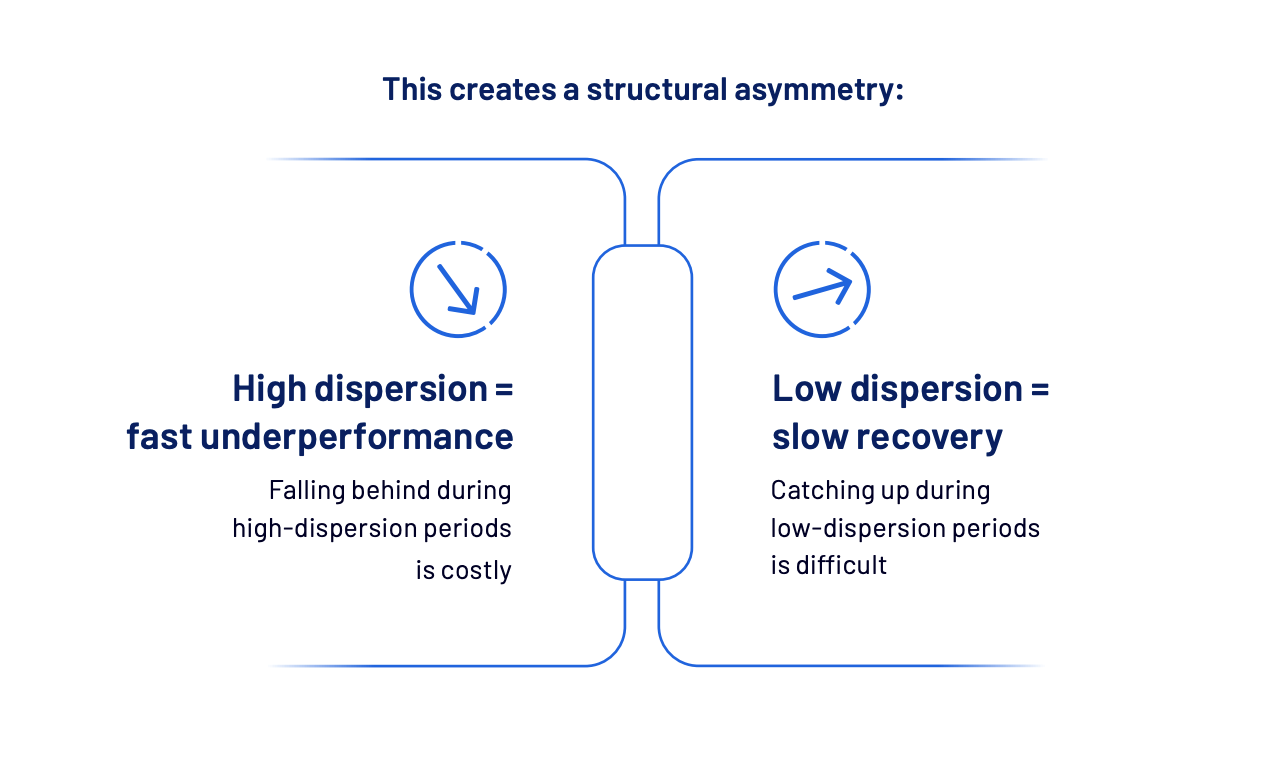

The Dispersion Trap occurs when a portfolio underperforms during a period of wide return dispersion, creating a wealth gap that becomes structurally difficult to close once dispersion compresses.

In these environments, performance differences are not evenly distributed across time. Instead, outcomes are often shaped during relatively short periods when dispersion expands. If a portfolio underperforms during those windows, the resulting wealth gap can become structurally difficult to reverse. Even if performance improves later, the opportunity to catch up may have already passed.

The Role of Compounding

The impact of dispersion becomes clear when viewed through the lens of compounding. A portfolio that falls behind during a high-dispersion period must generate excess returns on a smaller capital base. Even strong future performance may not be sufficient to close the gap. This asymmetric interaction between dispersion and compounding creates the Dispersion Trap, a powerful yet often underappreciated outcome.

Why This Matters for Investment Committees

Traditional performance evaluation focuses on policy benchmark comparisons and peer rankings. These frameworks are useful, but they implicitly assume that all underperformance is equally recoverable. In practice, it is not—and this assumption leads to systematically flawed conclusions.

Underperformance in a compressed-dispersion environment is fundamentally different from that in a wide-dispersion environment. The latter carries greater long-term consequences because it creates larger gaps in compounded wealth.

Without explicitly considering dispersion, these differences are difficult to detect. As a result, committees may underestimate the impact of certain periods of underperformance and overestimate their ability to recover from them.

Key questions:

- When did underperformance occur during high- or low-dispersion environments?

- Are performance differences driven by allocation or implementation?

- How wide was dispersion during periods of underperformance?

It’s clear that peer rankings and policy benchmarks alone are not enough. Committees should consider whether their analytics frameworks account for dispersion when evaluating portfolios.

Conclusion

Institutional portfolios do not need to look different to produce different outcomes. Dispersion ensures that even similar portfolios can diverge meaningfully over time. When performance gaps emerge during periods of elevated dispersion, compounding transforms small differences in annual returns into lasting gaps in institutional wealth. These gaps are not easily reversible. In many cases, they are permanent.

This reframes how investment committees should think about risk. The greatest risk is not short-term volatility or temporary underperformance; it is falling behind during periods of wide dispersion, when the opportunity cost of underperformance is highest.

The question for investment committees is not whether dispersion will create gaps, but whether their risk framework is designed to identify these environments, or whether they will only recognize the consequences after the wealth gap has already become effectively irreversible.